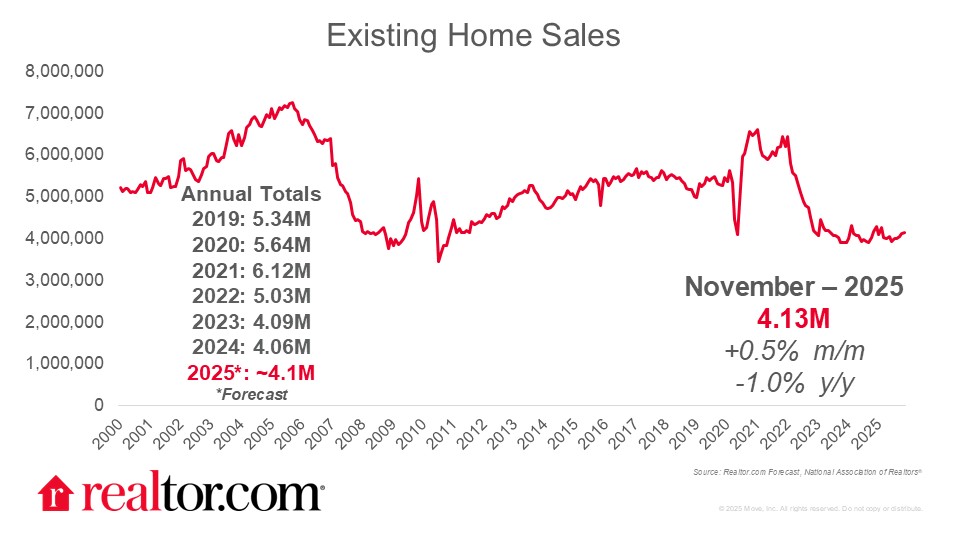

November 2025 existing-home sales

Existing-home sales built on their recent momentum in November, but did not fully exceed the higher year-ago pace. Existing-home sales rose 0.5% to 4.13M in November, from a slightly upwardly revised October estimate, but were down 1.0% from one year prior. Pending home sales rose in October yet also trailed the year-ago mark, as shoppers benefitted from seasonally favorable buying conditions and lower mortgage rates that have been more persistent than the dip in rates one year ago.

Mortgage rates finally relent, benefitting home shoppers

Mortgage rates were slow to relent in 2025, remaining above 6.5% until mid-September, providing a notable drag on earlier year home sales. November homebuyers, who would likely have gone under contract in September and October, benefited from rates near their lowest levels in a year, and fortunately, mortgage rates remain near this low level. In October, data showed that the mortgage rate tailwind was enough to offset any government-shutdown related slowing, and this was also true in November.

Home price growth slowed

Home sales price growth continued, with the median price climbing 1.2% from a year ago to $409,200, even as the typical asking price was down slightly in November. Notably, this was the slowest pace of home sales price growth since mid-2023, when prices declined from the prior year.

Pickup in home sales tightened the market, but balance improved versus one-year ago

Moderation in price growth was accompanied by a slight monthly decline in months supply to 4.2 months as sales picked up and inventory ebbed seasonally (down to 1.43M in November from 1.52M in October). Nonetheless, the inventory of unsold homes was still 7.5% higher than at this time last year, and months supply easily exceeded its year ago level (3.8 months). This shows that the housing market is still more balanced than it was, in line with our expectations for 2025 and 2026.

Regional variation reflects different housing supply constraints

Regionally, the Midwest saw the weakest sales performance and the highest price growth. It was the only region to see monthly decline (-2.0%) and saw the largest sales decline from one year prior (-3.0%) even as the median sales price rose 5.8%. This suggests that inventory constraints continue to play a role in this region, consistent with the Realtor.com finding that the count of actively for sale homes in the Midwest is one-third lower than was typical of the pre-pandemic period in November. Sales growth was stronger in the Northeast and South (up 4.1% and 1.1% in the month, respectively, and on par with the year ago pace for each) and prices also grew in these regions (up 1.1% and 0.8%, respectively). The West was the only region where the typical sales price softened (-0.9%) as November sales were flat from October and down 1.3% from the prior year.

Outlook suggests more improvement ahead

Looking ahead, my expectation is that mortgage rates remain near their current levels for most of 2026. This will be sufficient to bring about a very modest improvement in affordability, whether we’re measuring monthly payments outright or monthly payments relative to incomes. This should be enough to bump sales modestly higher in 2026, though they’ll remain historically low

{kind=link}